India’s eyewear market has long been fragmented, underpenetrated, and dominated by unorganized retail. Over the last decade, Lenskart has emerged as the most visible company attempting to formalize and digitize the category through an aggressive omnichannel strategy that combines online commerce, large-scale offline retail expansion, vertically integrated manufacturing, and consumer financing.

Its latest quarterly and annual performance indicates that the company’s growth engine remains strong. Revenue growth has accelerated significantly, supported by higher customer additions, international expansion, and increasing eyewear volumes. However, margins continue to face pressure as Lenskart invests heavily in scale, store expansion, supply chain infrastructure, and market penetration.

The results underscore a broader reality in India’s consumer internet and retail ecosystem: growth remains expensive, especially for companies balancing profitability with category leadership ambitions.

Revenue Momentum Remains Strong

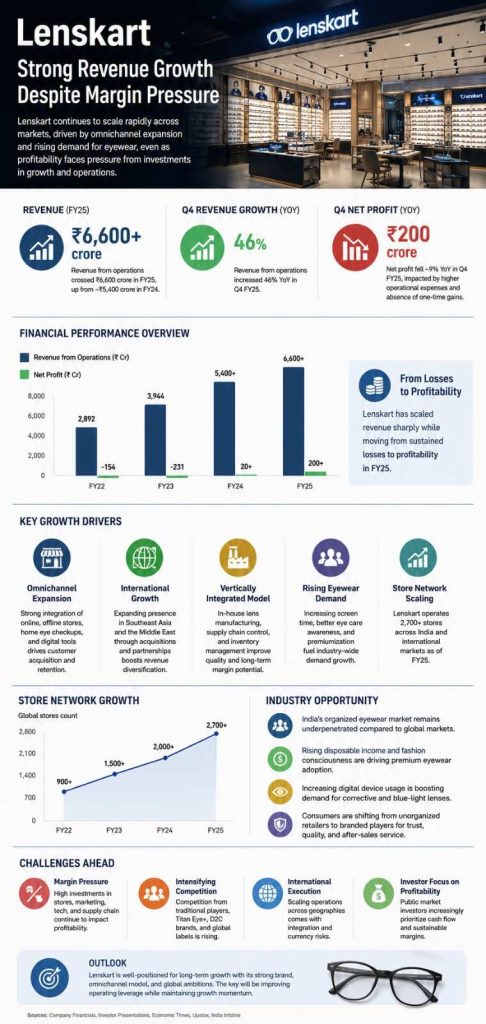

Lenskart reported a sharp rise in revenue during the latest quarter, with revenue from operations increasing approximately 46% year-on-year. The company attributed the growth primarily to strong volume expansion and new customer additions across both domestic and international markets.

Quarterly revenue reportedly crossed ₹2,500 crore during the January–March period, reflecting continued demand for prescription eyewear, sunglasses, and premium frames.

For the broader fiscal year, publicly available financial disclosures indicate that Lenskart’s revenue from operations crossed ₹6,600 crore in FY25, up from roughly ₹5,400 crore in FY24.

The scale of that growth is significant even within India’s fast-growing consumer startup ecosystem.

Unlike many digital-first brands that struggled after pandemic-era online demand normalized, Lenskart has benefited from a hybrid model where physical retail stores increasingly complement digital acquisition channels.

Industry analysts note that eyewear is structurally suited for omnichannel commerce because consumers often prefer in-person frame trials and eye testing before purchase. Lenskart’s store network has therefore become both a sales engine and a customer acquisition mechanism.

According to public filings and investor disclosures, the company expanded its store footprint to more than 2,700 locations globally by FY25.

Margin Pressure Reflects Expansion Costs

Despite strong top-line growth, profitability remains more nuanced.

Recent quarterly results showed a decline in net profit compared to the previous year, even as revenue expanded sharply. The company’s quarterly profit reportedly fell around 9% year-on-year to roughly ₹200 crore.

Part of the pressure came from the absence of one-time gains that benefited the prior-year period.

However, operational spending also continues to rise as Lenskart invests in:

- offline store expansion

- manufacturing capacity

- international acquisitions

- logistics and fulfillment

- technology infrastructure

- marketing and customer acquisition

This reflects a broader pattern visible across India’s retail-tech sector: companies that continue expanding aggressively are often sacrificing near-term margin expansion to secure long-term market share.

Lenskart’s operating structure is also fundamentally different from asset-light marketplaces.

Unlike horizontal ecommerce platforms, the company controls large parts of its value chain, including lens manufacturing, inventory management, retail operations, and optical services. While this creates stronger quality control and potentially higher long-term margins, it also increases operational intensity and capital requirements.

Several analysts tracking the retail sector believe the company is currently prioritizing scale efficiencies over short-term earnings optimization.

Omnichannel Retail Is Becoming Lenskart’s Biggest Advantage

One of the most important aspects of Lenskart’s business model is its omnichannel integration.

The company was among the earliest Indian consumer startups to aggressively combine:

- online ordering

- home eye checkups

- offline experience stores

- app-based recommendations

- AI-assisted frame selection

- vertically integrated manufacturing

This model helped the company reduce dependence on third-party optical retailers while building a recognizable consumer brand.

In India’s eyewear market, trust and physical interaction remain important purchase drivers. Consumers often need eye testing, frame fitting, or after-sales adjustments — areas where purely online players face limitations.

Lenskart’s offline network therefore functions as both a revenue channel and a retention mechanism.

The company has also benefited from increasing consumer willingness to purchase premium eyewear products, including blue-light lenses, lightweight frames, and branded sunglasses.

That premiumization trend has strengthened across urban India over the last five years, particularly among younger consumers and working professionals.

International Markets Are Contributing More to Growth

Another major driver of Lenskart’s expansion has been its growing international presence.

The company has expanded into Southeast Asia and the Middle East through acquisitions, partnerships, and local retail expansion initiatives.

International growth has become strategically important for two reasons:

1. Larger Addressable Market

India remains a large but price-sensitive eyewear market. International expansion allows Lenskart to target consumers with higher average order values.

2. Diversified Revenue Base

Geographic diversification reduces dependence on a single market and creates opportunities for manufacturing scale advantages.

However, international operations also introduce integration challenges, currency exposure, and execution complexity.

Analysts caution that sustaining margins while expanding internationally will require disciplined operational management.

India’s Eyewear Market Still Has Significant Headroom

Lenskart’s growth also reflects broader structural shifts in India’s optical retail market.

The organized eyewear industry remains relatively underpenetrated compared to developed economies.

Several factors continue to support long-term category growth:

Rising Screen Time

Increased digital device usage has accelerated demand for corrective eyewear and blue-light protection lenses.

Growing Disposable Income

Urban consumers are increasingly treating eyewear as both a utility and a fashion accessory.

Better Awareness Around Eye Care

Routine eye testing and preventive eye care awareness are improving, especially in Tier 1 and Tier 2 cities.

Shift Toward Branded Products

Consumers are gradually moving away from unorganized optical stores toward branded retail chains offering warranties, financing, and standardized quality.

Industry estimates from various market research firms have consistently projected India’s eyewear market to grow at a healthy pace over the coming decade, though exact forecasts vary significantly depending on methodology.

Profitability Remains the Key Investor Question

Even though Lenskart has shown substantial operational progress, investors remain focused on one central question: how sustainable are its margins at scale?

The debate is especially relevant in the current startup funding environment, where public and private market investors increasingly prioritize cash flow discipline over pure growth metrics.

Some analysts argue that Lenskart’s vertically integrated model could eventually generate stronger operating leverage as store density increases and manufacturing utilization improves.

Others remain cautious because offline retail expansion remains expensive and customer acquisition costs in consumer brands continue to rise.

Public market scrutiny has also intensified following the company’s IPO-related developments and broader investor expectations around sustainable profitability.

Recent discussions among retail investors and market observers have highlighted concerns around valuation multiples and the quality of earnings adjustments, particularly regarding one-time gains and accounting-driven profitability improvements.

Still, compared to many consumer-tech startups, Lenskart’s financial trajectory appears more mature.

The company has moved from sustained losses in earlier years toward profitability while continuing to grow aggressively.

That balance is relatively rare within India’s venture-backed retail ecosystem.

Competition Is Intensifying

Lenskart’s leadership position does not guarantee long-term dominance.

The company faces competition from:

- traditional optical chains

- regional retailers

- fashion eyewear brands

- ecommerce marketplaces

- premium international labels

Established players such as Titan Company through its Eye+ business continue expanding aggressively in organized optical retail.

At the same time, global eyewear trends are increasingly influencing Indian consumer preferences, particularly in premium and fashion-led categories.

The competitive landscape may become even more crowded as international brands deepen their India presence and domestic D2C brands scale operations.

Future Outlook: Scale vs Efficiency

Lenskart now appears to be entering a more complex phase of growth.

Its earlier challenge was proving that eyewear could become a large-scale organized retail category in India. That question has largely been answered.

The next challenge is demonstrating that large-scale omnichannel expansion can consistently generate durable margins.

Key indicators investors and analysts will likely monitor over the coming quarters include:

- same-store sales growth

- international profitability

- customer retention

- EBITDA margin trajectory

- store-level economics

- manufacturing efficiency

- free cash flow generation

If Lenskart can improve operating leverage while maintaining strong customer growth, it could strengthen its position as one of India’s most significant consumer retail technology companies.

But if margin pressure persists despite scale expansion, investor expectations may gradually shift toward slower, more disciplined growth.

Conclusion

Lenskart’s latest performance reinforces its position as one of India’s strongest consumer retail growth stories.

The company continues to expand rapidly across markets, deepen its omnichannel presence, and formalize a historically fragmented industry. Revenue growth remains robust, customer acquisition momentum appears strong, and brand recall continues to improve.

At the same time, the financial results highlight the operational complexity of scaling a vertically integrated retail business.

The central question is no longer whether Lenskart can grow. It is whether the company can sustain growth while delivering consistent profitability in an increasingly competitive and margin-sensitive environment.

That balance will likely define the company’s next phase of evolution.

Also Read : How Indian Startups Are Replacing Middle Management With Automation

Add Startup Times as a preferred Source on Google – Click Here

Last Updated on Thursday, May 21, 2026 2:32 pm by Startup Times